Here we are in yet another new year. The obligations and celebrations are over. Chances are, you’ve spent a fair amount over the holidays and might need a plan to help kickstart 2025 with some actionable financial goals. Here are a few ideas.

Create a Budget

This one never gets old. Why? It’s one of the keys to successful budgeting. You can set up a budget for the year that includes essentials, entertainment, and nice-to-haves, aka your Wish Farm. Then place it in your planner or app – there are many good ones out there. In fact, there’s a TikTok trend called loud budgeting, where people openly discuss their financial goals on social media – why they do or don’t want to buy something. If this is your thing and it helps you stay on track, go for it! If not, a good old-fashioned planner works just as well.

Bucket Your Money

This is the next step after the aforementioned. Split your money into categories: food, rent/ mortgage, utilities, medical, entertainment, vacation, etc. Apps can help you parse out these groups. You might also set up separate banking accounts for some of the necessities so you’ll know to leave them alone and not dip into them, tempting as it may be.

Set Up Auto-Drafts

Let’s say you’re saving for your child’s college fund or a down payment on a car. When you create an auto-draft for a certain amount, you’ll never miss that deposit. If you need to tweak the amount during the year, do it. Here’s the bottom line: 1) You’ll learn to live on less, and 2) you’ll be on the way to making your dreams come true.

Look for Savings Deals

Don’t just settle for the interest rate your current bank is offering. There are many options out there to grow your money. But first, do you want to lock into a fixed rate? This can be useful for long-term goals, such as buying a property. Or do you want an easy-to-access account with the ability to withdraw cash for emergencies or short-term needs like birthday or wedding gifts? Shop around.

Cancel Seldom-Used Subscriptions

Scour your bank statement. Do you need all those online magazine subscriptions? How about newsletters you pay for – the ones you rarely read? Purge your subscriptions, then see how much you’ll save. If you’re so inclined, you could put these dollars toward a gym membership. January is when all the specials appear: zero joining fees, if not a seriously cut rate.

Start a Savings Challenge

Try putting away a small amount every month. Get in the habit of emptying your pockets or coin purse. Safeguard your coins in a mason jar, and then transfer them monthly into your savings account. The next month, increase how much you contribute. Pennies, nickels, dimes, and quarters add up! After a year, you might be surprised how much you’ve saved.

Decide on Goals

These can be small or large. It’s up to you. Spend some time thinking about what’s important. Do you want to remodel your house? Contribute to a beloved charity or cause? One resource you might want to consider setting up is an emergency spending pot. This is essential and sometimes overlooked. Regardless of what you decide, figure out your parameters: how much to set aside, how often, and by when. Having financial targets gives you something to look forward to. Best of all, when you achieve your goal, it’s an awesome feeling.

More often than not, New Year’s resolutions center on getting physically fit. But if you stay the course with your finances, you’ll most definitely be, wait for it … fiscally fit!

Sources

10 things you can do right now to start 2025 with fresh finances

Here we are in yet another new year. The obligations and celebrations are over. Chances are, you’ve spent a fair amount over the holidays and might need a plan to help kickstart 2025 with some actionable financial goals. Here are a few ideas.

Create a Budget

This one never gets old. Why? It’s one of the keys to successful budgeting. You can set up a budget for the year that includes essentials, entertainment, and nice-to-haves, aka your Wish Farm. Then place it in your planner or app – there are many good ones out there. In fact, there’s a TikTok trend called loud budgeting, where people openly discuss their financial goals on social media – why they do or don’t want to buy something. If this is your thing and it helps you stay on track, go for it! If not, a good old-fashioned planner works just as well.

Bucket Your Money

This is the next step after the aforementioned. Split your money into categories: food, rent/ mortgage, utilities, medical, entertainment, vacation, etc. Apps can help you parse out these groups. You might also set up separate banking accounts for some of the necessities so you’ll know to leave them alone and not dip into them, tempting as it may be.

Set Up Auto-Drafts

Let’s say you’re saving for your child’s college fund or a down payment on a car. When you create an auto-draft for a certain amount, you’ll never miss that deposit. If you need to tweak the amount during the year, do it. Here’s the bottom line: 1) You’ll learn to live on less, and 2) you’ll be on the way to making your dreams come true.

Look for Savings Deals

Don’t just settle for the interest rate your current bank is offering. There are many options out there to grow your money. But first, do you want to lock into a fixed rate? This can be useful for long-term goals, such as buying a property. Or do you want an easy-to-access account with the ability to withdraw cash for emergencies or short-term needs like birthday or wedding gifts? Shop around.

Cancel Seldom-Used Subscriptions

Scour your bank statement. Do you need all those online magazine subscriptions? How about newsletters you pay for – the ones you rarely read? Purge your subscriptions, then see how much you’ll save. If you’re so inclined, you could put these dollars toward a gym membership. January is when all the specials appear: zero joining fees, if not a seriously cut rate.

Start a Savings Challenge

Try putting away a small amount every month. Get in the habit of emptying your pockets or coin purse. Safeguard your coins in a mason jar, and then transfer them monthly into your savings account. The next month, increase how much you contribute. Pennies, nickels, dimes, and quarters add up! After a year, you might be surprised how much you’ve saved.

Decide on Goals

These can be small or large. It’s up to you. Spend some time thinking about what’s important. Do you want to remodel your house? Contribute to a beloved charity or cause? One resource you might want to consider setting up is an emergency spending pot. This is essential and sometimes overlooked. Regardless of what you decide, figure out your parameters: how much to set aside, how often, and by when. Having financial targets gives you something to look forward to. Best of all, when you achieve your goal, it’s an awesome feeling.

More often than not, New Year’s resolutions center on getting physically fit. But if you stay the course with your finances, you’ll most definitely be, wait for it … fiscally fit!

Sources

10 things you can do right now to start 2025 with fresh finances

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

Improving Federal Building Security Act of 2024 (S 3613) – The Federal Protective Service (FPS) contracts security guards to control access to government facilities and screen visitors to detect prohibited items, such as pepper spray and batons. Earlier this year, FPS investigators conducted a covert test at certain federal buildings in which the guards failed to detect prohibited items about 50 percent of the time. In response, Congress passed this bill requiring Facility Security Committees to respond to security recommendations issued by the FPS. It also mandates that the Homeland Security Department submit an unredacted report to Congress regarding FPS surveillance technology recommendations as well as summarize the FPS recommendations that buildings accepted or rejected. However, no additional funding for security is appropriated by the bill, which will sunset five years following enactment. The act was introduced on Jan. 18, 2024, by Sen. Gary Peters (D-MI). It passed in the Senate on March 23, the House on Dec. 10, and was signed into law on Dec. 17.

Servicemember Quality of Life Improvement and National Defense Authorization Act for Fiscal Year 2025 (HR 5009) – This year’s version of the annual funding bill features a 14.5 percent increase in pay for junior enlisted servicemembers, as well as a 4.5 percent pay raise for all other personnel. The legislation also provides cost-of-living allowances per location, improved housing/barracks repair programs, more access to medical and mental health services, and increased employment support for military spouses. The legislation was introduced by Rep. David Joyce (R-OH) on July 27, 2023. This is a bipartisan bill that has passed in both the Senate and the House with various changes. It is currently awaiting signature by the White House for enactment.

Coastal Habitat Conservation Act of 2023 (HR 2950) – Introduced by Rep. Jared Huffman (D-CA) on April 7, 2023, this bill passed the House on Sept. 24, 2024, the Senate on Nov. 21, and was signed into law on Dec. 11. The legislation empowers the Coastal Program of the United States Fish and Wildlife Service to increase efforts to assess, protect, restore and enhance key coastal environments that provide fish and wildlife habitats for certain federal trust species.

Thomas R. Carper Water Resources Development Act of 2024 (S 4367) – This legislation was introduced by Sen. Thomas Carper (D-DE) on May 20, 2024. It passed in the Senate on Aug. 1 and in the House (with changes) on Dec. 10; the final bill is expected to be approved and signed into law by the end of the congressional session. This bipartisan bill is designed to improve the nation’s water resources infrastructure, including ports and harbors, inland waterway navigation, and flood and storm protection; it also strengthens our resilience during natural disasters. The legislation also institutes reforms at the U.S. Army Corps of Engineers in order to streamline processes and deploy projects faster.

SHIELD Against CCP Act (HR 9668) – Introduced on Sept. 18, 2024, by Rep. Dale Strong (R-AL), this bill would establish a task force working with the Department of Homeland Security. The group’s sole focus would be on countering terrorism, cybersecurity, and border/port security related to threats posed by the Chinese Communist Party. The legislation is in response to recent CCP activities such as stealing intellectual property and technology, threats to economic supply chain security and critical infrastructure, and surveillance activities targeting U.S. defense sites and even American citizens. The bipartisan bill passed in the House on Dec. 10 and is currently in the Senate.

Increasing Baseline Updates Act (HR 9716) – In the first quarter of each year, the Congressional Budget Office provides Congress with an annual baseline 10-year projection of the budget and economy based on the fiscal impact of legislative proposals. Updates are released in Q2 and Q3 to reflect newly enacted laws and economic conditions. This bill would mandate that the executive branch provide critical data to the CBO by February 1 of each year to produce a more accurate annual budget baseline. The bill passed in the House on Dec. 11 and currently lies with the Senate. It was introduced by Rep. Blake Moore (R-UT) on Sept. 20, 2024.

National Security

January 1, 2025 · Blog, Congress at Work

⏱ 4 min read

Improving Federal Building Security Act of 2024 (S 3613) – The Federal Protective Service (FPS) contracts security guards to control access to government facilities and screen visitors to detect prohibited items, such as pepper spray and batons. Earlier this year, FPS investigators conducted a covert test at certain federal buildings in which the guards failed to detect prohibited items about 50 percent of the time. In response, Congress passed this bill requiring Facility Security Committees to respond to security recommendations issued by the FPS. It also mandates that the Homeland Security Department submit an unredacted report to Congress regarding FPS surveillance technology recommendations as well as summarize the FPS recommendations that buildings accepted or rejected. However, no additional funding for security is appropriated by the bill, which will sunset five years following enactment. The act was introduced on Jan. 18, 2024, by Sen. Gary Peters (D-MI). It passed in the Senate on March 23, the House on Dec. 10, and was signed into law on Dec. 17.

Servicemember Quality of Life Improvement and National Defense Authorization Act for Fiscal Year 2025 (HR 5009) – This year’s version of the annual funding bill features a 14.5 percent increase in pay for junior enlisted servicemembers, as well as a 4.5 percent pay raise for all other personnel. The legislation also provides cost-of-living allowances per location, improved housing/barracks repair programs, more access to medical and mental health services, and increased employment support for military spouses. The legislation was introduced by Rep. David Joyce (R-OH) on July 27, 2023. This is a bipartisan bill that has passed in both the Senate and the House with various changes. It is currently awaiting signature by the White House for enactment.

Coastal Habitat Conservation Act of 2023 (HR 2950) – Introduced by Rep. Jared Huffman (D-CA) on April 7, 2023, this bill passed the House on Sept. 24, 2024, the Senate on Nov. 21, and was signed into law on Dec. 11. The legislation empowers the Coastal Program of the United States Fish and Wildlife Service to increase efforts to assess, protect, restore and enhance key coastal environments that provide fish and wildlife habitats for certain federal trust species.

Thomas R. Carper Water Resources Development Act of 2024 (S 4367) – This legislation was introduced by Sen. Thomas Carper (D-DE) on May 20, 2024. It passed in the Senate on Aug. 1 and in the House (with changes) on Dec. 10; the final bill is expected to be approved and signed into law by the end of the congressional session. This bipartisan bill is designed to improve the nation’s water resources infrastructure, including ports and harbors, inland waterway navigation, and flood and storm protection; it also strengthens our resilience during natural disasters. The legislation also institutes reforms at the U.S. Army Corps of Engineers in order to streamline processes and deploy projects faster.

SHIELD Against CCP Act (HR 9668) – Introduced on Sept. 18, 2024, by Rep. Dale Strong (R-AL), this bill would establish a task force working with the Department of Homeland Security. The group’s sole focus would be on countering terrorism, cybersecurity, and border/port security related to threats posed by the Chinese Communist Party. The legislation is in response to recent CCP activities such as stealing intellectual property and technology, threats to economic supply chain security and critical infrastructure, and surveillance activities targeting U.S. defense sites and even American citizens. The bipartisan bill passed in the House on Dec. 10 and is currently in the Senate.

Increasing Baseline Updates Act (HR 9716) – In the first quarter of each year, the Congressional Budget Office provides Congress with an annual baseline 10-year projection of the budget and economy based on the fiscal impact of legislative proposals. Updates are released in Q2 and Q3 to reflect newly enacted laws and economic conditions. This bill would mandate that the executive branch provide critical data to the CBO by February 1 of each year to produce a more accurate annual budget baseline. The bill passed in the House on Dec. 11 and currently lies with the Senate. It was introduced by Rep. Blake Moore (R-UT) on Sept. 20, 2024.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

The Salt Typhoon cyberattack is among recent cyberattacks that reaffirm the urgent need for robust data security measures. This attack targeted major telecommunications providers, compromising critical infrastructure and potentially exposing vast amounts of sensitive data. With cyberthreats becoming more sophisticated, businesses and individuals must prioritize data security to maintain trust and compliance.

The Role of Apps in Managing and Protecting Client Data

Businesses need apps because they make the work easier and more organized. Apps help teams communicate better, manage tasks, and share information quickly, no matter where people are. The apps also simplify handling customer needs, improving service, and tracking business performance. Generally, apps save time while helping businesses work smarter and stay competitive.

One of the most critical uses of apps is managing client data. This data includes personal details like names and addresses. It also includes financial information such as bank details, as well as business-specific data like contracts and project plans. Losing or exposing this sensitive information can lead to severe consequences, including financial losses, legal penalties, and damaged reputations. Clients may lose trust in your business, leading to lost opportunities and reduced customer loyalty. By using apps effectively, businesses can better organize, safeguard, and utilize client data to build stronger relationships and maintain long-term success.

Encryption: A Critical Security Measure

Encryption has become crucial in modern data security. It transforms readable data into an unreadable format, ensuring only authorized parties can access the information. There are various types of encryptions, including end-to-end encryption (E2EE), which protects data during transmission, and at-rest encryption, which secures stored data.

Following the Salt Typhoon cyberattacks, the FBI and Cybersecurity and Infrastructure Security Agency (CISA) issued a joint advisory urging individuals and organizations to prioritize using encrypted communication channels. Given the vulnerability of traditional communication methods, the agencies strongly recommended adopting end-to-end encrypted messaging apps like Signal for secure communication. This recommendation aims to mitigate the risks associated with compromised telecommunication networks. It also helps protect sensitive information from unauthorized access. Even if cybercriminals intercept the data, they cannot decipher it without the encryption key. This layer of protection mitigates the risks of unauthorized access and data breaches, making encryption an essential tool for businesses.

The Role of Encrypted Apps

Enhanced security: Encrypted apps provide a critical layer of defense against sophisticated cyberattacks. By encrypting data both in transit and at rest, these apps ensure that even if communication networks are compromised, sensitive information remains inaccessible to attackers.

Compliance with regulations: With so many ongoing cyberattacks, regulatory scrutiny of data security practices has intensified. Encrypted apps can help businesses comply with relevant regulations, such as the GDPR and CCPA, by demonstrating a commitment to data protection.

Building trust and customer loyalty: Customers are increasingly wary of data breaches in an era of heightened cybersecurity concerns. Utilizing encrypted apps demonstrates a commitment to data security and privacy, fostering trust and loyalty among clients.

Protecting business operations: Encrypted apps are crucial for protecting client data and safeguarding critical business information, such as intellectual property, financial records, and internal communications. This ensures the continuity and integrity of business operations, even in the face of advanced cyber threats.

Choosing and Implementing Encrypted Apps

When selecting and implementing the right encrypted apps, it is important to consider them carefully. First, it is good to consider industry-specific needs as different industries have different data security needs. For example, while a healthcare provider must comply with Health Insurance Portability and Accountability Act (HIPAA) regulations, a business in the financial industry must adhere to banking regulations. This calls for selecting industry-specific apps.

Businesses also must prioritize apps with robust security features, such as strong encryption algorithms, multifactor authentication, and regular security updates. It is also important to carefully review the data privacy policies of app providers and ensure compliance with relevant regulations.

Effective employee training is also essential for successfully implementing encrypted apps. Employees must be educated on the importance of data security, the proper use of encrypted apps, and best practices for handling sensitive information.

Conclusion

Client data is one of a business’s most valuable assets, and protecting it is paramount. The growing threat of cyberattacks and the increasing complexity of data protection regulations make encryption an essential tool. By embracing encrypted communication channels, businesses can significantly enhance their resilience against sophisticated cyberattacks, protect sensitive client data, and maintain a competitive edge in today’s digital economy.

Securing Client Data: The Importance of Encrypted Apps

January 1, 2025 · Blog, What's New in Technology

⏱ 4 min read

The Salt Typhoon cyberattack is among recent cyberattacks that reaffirm the urgent need for robust data security measures. This attack targeted major telecommunications providers, compromising critical infrastructure and potentially exposing vast amounts of sensitive data. With cyberthreats becoming more sophisticated, businesses and individuals must prioritize data security to maintain trust and compliance.

The Role of Apps in Managing and Protecting Client Data

Businesses need apps because they make the work easier and more organized. Apps help teams communicate better, manage tasks, and share information quickly, no matter where people are. The apps also simplify handling customer needs, improving service, and tracking business performance. Generally, apps save time while helping businesses work smarter and stay competitive.

One of the most critical uses of apps is managing client data. This data includes personal details like names and addresses. It also includes financial information such as bank details, as well as business-specific data like contracts and project plans. Losing or exposing this sensitive information can lead to severe consequences, including financial losses, legal penalties, and damaged reputations. Clients may lose trust in your business, leading to lost opportunities and reduced customer loyalty. By using apps effectively, businesses can better organize, safeguard, and utilize client data to build stronger relationships and maintain long-term success.

Encryption: A Critical Security Measure

Encryption has become crucial in modern data security. It transforms readable data into an unreadable format, ensuring only authorized parties can access the information. There are various types of encryptions, including end-to-end encryption (E2EE), which protects data during transmission, and at-rest encryption, which secures stored data.

Following the Salt Typhoon cyberattacks, the FBI and Cybersecurity and Infrastructure Security Agency (CISA) issued a joint advisory urging individuals and organizations to prioritize using encrypted communication channels. Given the vulnerability of traditional communication methods, the agencies strongly recommended adopting end-to-end encrypted messaging apps like Signal for secure communication. This recommendation aims to mitigate the risks associated with compromised telecommunication networks. It also helps protect sensitive information from unauthorized access. Even if cybercriminals intercept the data, they cannot decipher it without the encryption key. This layer of protection mitigates the risks of unauthorized access and data breaches, making encryption an essential tool for businesses.

The Role of Encrypted Apps

Enhanced security: Encrypted apps provide a critical layer of defense against sophisticated cyberattacks. By encrypting data both in transit and at rest, these apps ensure that even if communication networks are compromised, sensitive information remains inaccessible to attackers.

Compliance with regulations: With so many ongoing cyberattacks, regulatory scrutiny of data security practices has intensified. Encrypted apps can help businesses comply with relevant regulations, such as the GDPR and CCPA, by demonstrating a commitment to data protection.

Building trust and customer loyalty: Customers are increasingly wary of data breaches in an era of heightened cybersecurity concerns. Utilizing encrypted apps demonstrates a commitment to data security and privacy, fostering trust and loyalty among clients.

Protecting business operations: Encrypted apps are crucial for protecting client data and safeguarding critical business information, such as intellectual property, financial records, and internal communications. This ensures the continuity and integrity of business operations, even in the face of advanced cyber threats.

Choosing and Implementing Encrypted Apps

When selecting and implementing the right encrypted apps, it is important to consider them carefully. First, it is good to consider industry-specific needs as different industries have different data security needs. For example, while a healthcare provider must comply with Health Insurance Portability and Accountability Act (HIPAA) regulations, a business in the financial industry must adhere to banking regulations. This calls for selecting industry-specific apps.

Businesses also must prioritize apps with robust security features, such as strong encryption algorithms, multifactor authentication, and regular security updates. It is also important to carefully review the data privacy policies of app providers and ensure compliance with relevant regulations.

Effective employee training is also essential for successfully implementing encrypted apps. Employees must be educated on the importance of data security, the proper use of encrypted apps, and best practices for handling sensitive information.

Conclusion

Client data is one of a business’s most valuable assets, and protecting it is paramount. The growing threat of cyberattacks and the increasing complexity of data protection regulations make encryption an essential tool. By embracing encrypted communication channels, businesses can significantly enhance their resilience against sophisticated cyberattacks, protect sensitive client data, and maintain a competitive edge in today’s digital economy.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

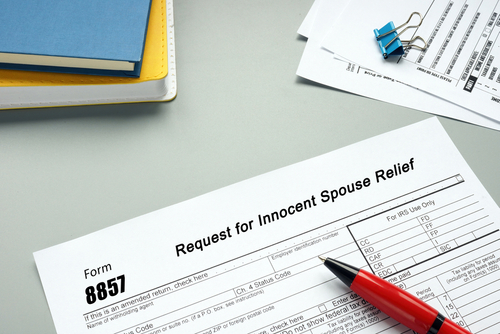

The word “innocent” in innocent spouse relief can be misleading. It doesn’t imply you’re perfect or blameless – it’s more about whether you knew or should have known about the tax issue. The IRS defines “innocence” in a specific way, and it hinges on the concept of reasonable ignorance. In short, the issue isn’t one of morality; it’s about whether you could have reasonably been unaware of a tax problem.

Innocent spouse relief allows you to avoid being held responsible for tax debts, penalties, and interest stemming from a joint tax filing. In the case that a spouse (or ex-spouse) made an error that led to a tax issue, regardless of intention, you may not have to shoulder the burden. Say your income wasn’t reported, excessive deductions were claimed, or tax fraud was committed. If you meet the IRS criteria, you can request relief by submitting Form 8857.

Qualifications for Innocent Spouse Relief

To qualify, you must meet several conditions.

Joint Tax Return: The tax liability must arise from a joint return. When you file together, both spouses are equally responsible for any tax issues that arise.

Tax Underreporting: The tax issue must stem from underreported income or an incorrect claim for deductions or credits. This could involve unreported income (like from offshore accounts) or fraudulent deductions made by your spouse.

Lack of Knowledge: You must show that, at the time of filing, you were unaware of the problem and had no reason to suspect it.

Unfair Responsibility: Lastly, it must be deemed unjust to hold you liable. The IRS looks at factors such as whether you benefited from the underreported taxes (e.g., through extravagant spending) or if you’ve divorced.

What Doesn’t Qualify for Innocent Spouse Relief?

Not all cases involving a spouse’s financial mismanagement qualify for relief. The IRS may reject your claim in the following situations:

Awareness of the Mistake: If you knew about the issue or should have known, you won’t be eligible for relief. Simply stating that you didn’t read the return won’t suffice. The IRS expects you to recognize obvious errors if you have access to the relevant information.

Divorce Doesn’t Automatically Provide Relief: Divorce alone doesn’t eliminate your liability for tax debt. Joint returns create shared responsibility, and being separated or divorced doesn’t mean the IRS will automatically release you from this obligation. You must prove your innocence through the relief process.

Disagreements Over Personal Spending: If your spouse’s spending decisions are something you disagree with, the IRS will not consider it a tax issue unless it involves unreported income or fraudulent deductions. The IRS focuses on tax matters, not marital conflicts over financial choices.

Pros and Cons of Filing

Advantages include:

Avoid Financial Hardship: Tax liabilities, along with interest and penalties, can be overwhelming. Innocent spouse relief can protect you from these financial burdens.

Clear Your Name: If you’ve been unfairly tied to a tax issue you didn’t cause, the relief process can help remove you from the responsibility.

Peace of Mind: Successfully claiming relief can bring emotional relief, especially if you’ve gone through a challenging marriage.

Potential drawbacks are:

No Guarantee of Approval: The IRS does not grant relief easily. You’ll need to provide strong evidence, and the process can be lengthy and difficult.

Time Limitations: You generally must apply for relief within two years of the IRS starting collection efforts. Missing this deadline could result in losing the opportunity for relief.

Invasive Process: The IRS will closely examine your financial and personal life, including details about your marriage and finances, which could feel intrusive if you value your privacy.

Possible Strain on Relationships: If you’re still married, filing for relief could cause tension, as it might be seen as blaming your spouse for the tax issue.

Conclusion

To request innocent spouse relief, you’ll need to file Form 8857. Be prepared to provide details about the tax years involved, explain why you didn’t know about the issue, and any supporting documents (like bank statements, emails, or divorce decrees.

After submitting the form, the IRS will notify your spouse or ex-spouse, who will have a chance to respond by a specific date.

What is Innocent Spouse Relief?

January 1, 2025 · Blog, Tax and Financial News

⏱ 4 min read

The word “innocent” in innocent spouse relief can be misleading. It doesn’t imply you’re perfect or blameless – it’s more about whether you knew or should have known about the tax issue. The IRS defines “innocence” in a specific way, and it hinges on the concept of reasonable ignorance. In short, the issue isn’t one of morality; it’s about whether you could have reasonably been unaware of a tax problem.

Innocent spouse relief allows you to avoid being held responsible for tax debts, penalties, and interest stemming from a joint tax filing. In the case that a spouse (or ex-spouse) made an error that led to a tax issue, regardless of intention, you may not have to shoulder the burden. Say your income wasn’t reported, excessive deductions were claimed, or tax fraud was committed. If you meet the IRS criteria, you can request relief by submitting Form 8857.

Qualifications for Innocent Spouse Relief

To qualify, you must meet several conditions.

Joint Tax Return: The tax liability must arise from a joint return. When you file together, both spouses are equally responsible for any tax issues that arise.

Tax Underreporting: The tax issue must stem from underreported income or an incorrect claim for deductions or credits. This could involve unreported income (like from offshore accounts) or fraudulent deductions made by your spouse.

Lack of Knowledge: You must show that, at the time of filing, you were unaware of the problem and had no reason to suspect it.

Unfair Responsibility: Lastly, it must be deemed unjust to hold you liable. The IRS looks at factors such as whether you benefited from the underreported taxes (e.g., through extravagant spending) or if you’ve divorced.

What Doesn’t Qualify for Innocent Spouse Relief?

Not all cases involving a spouse’s financial mismanagement qualify for relief. The IRS may reject your claim in the following situations:

Awareness of the Mistake: If you knew about the issue or should have known, you won’t be eligible for relief. Simply stating that you didn’t read the return won’t suffice. The IRS expects you to recognize obvious errors if you have access to the relevant information.

Divorce Doesn’t Automatically Provide Relief: Divorce alone doesn’t eliminate your liability for tax debt. Joint returns create shared responsibility, and being separated or divorced doesn’t mean the IRS will automatically release you from this obligation. You must prove your innocence through the relief process.

Disagreements Over Personal Spending: If your spouse’s spending decisions are something you disagree with, the IRS will not consider it a tax issue unless it involves unreported income or fraudulent deductions. The IRS focuses on tax matters, not marital conflicts over financial choices.

Pros and Cons of Filing

Advantages include:

Avoid Financial Hardship: Tax liabilities, along with interest and penalties, can be overwhelming. Innocent spouse relief can protect you from these financial burdens.

Clear Your Name: If you’ve been unfairly tied to a tax issue you didn’t cause, the relief process can help remove you from the responsibility.

Peace of Mind: Successfully claiming relief can bring emotional relief, especially if you’ve gone through a challenging marriage.

Potential drawbacks are:

No Guarantee of Approval: The IRS does not grant relief easily. You’ll need to provide strong evidence, and the process can be lengthy and difficult.

Time Limitations: You generally must apply for relief within two years of the IRS starting collection efforts. Missing this deadline could result in losing the opportunity for relief.

Invasive Process: The IRS will closely examine your financial and personal life, including details about your marriage and finances, which could feel intrusive if you value your privacy.

Possible Strain on Relationships: If you’re still married, filing for relief could cause tension, as it might be seen as blaming your spouse for the tax issue.

Conclusion

To request innocent spouse relief, you’ll need to file Form 8857. Be prepared to provide details about the tax years involved, explain why you didn’t know about the issue, and any supporting documents (like bank statements, emails, or divorce decrees.

After submitting the form, the IRS will notify your spouse or ex-spouse, who will have a chance to respond by a specific date.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

The CAC Payback Period looks at how a business needs to recover its investment in attracting new customers. It is especially crucial for companies that are in industries with large marketing and sales costs. It’s an important metric because it helps businesses measure their performance in a number of ways.

First, it shows how well a business is managing its budget. Based on the resulting figure of the CAC Payback Period, the shorter the time required to break even on its customer acquisition costs, the more efficient a company is with its sales and marketing expenses. If, however, the result is high, this signals the company is doing something wrong and needs to analyze its current approach.

Running this analysis can also identify a company’s financial perils. The more prolonged the CAC Payback Period, the more likely a company might be facing cash flow concerns. Whether it is caused by overall economic conditions or industry or company-specific challenges, this is another reason for a company to run the numbers to see how it can mitigate or turn around the costs associated with acquiring customers.

The calculation also can help a business determine if it is able to expand to new products and markets and scale up existing product lines. The shorter the time needed to acquire new customers, the more likely a business can grow.

When investors and lenders analyze a company’s financials, including this metric, the more efficient a company is, and the more likely it will attract investors or have lenders offer favorable financing terms.

How to Calculate the CAC Payback Period

This scenario looks at $300,000 in customer acquisition costs, such as marketing, sales, etc., for a three-month period. The company obtained 1,000 new customers and is expected to gain $200,000 in new monthly recurring revenue (MRR), with an estimated gross margin of 60 percent.

First Step: Calculate the CAC by dividing Sales and Marketing Expenses by the new customers (1,000). It’s expressed as follows:

CAC = Sales and Marketing Expenses/Number of New Customers

CAC = $300,000/1,000 = $300 per customer

Second Step: This is to determine the monthly recurring revenue (MRR) per customer. The new MRR amount is divided by the number of newly acquired customers. It’s calculated as follows:

MRR = $200,000/1,000 = $200 per customer

Third Step: Determine the gross margin or how much remains from revenue after subtracting direct costs. In this case, we’ll use 60 percent.

Fourth (and Final) Step: This step determines how many months it will take to recoup the customer acquisition costs from the profits generated by the newly acquired customer. It’s calculated as follows:

CAC Payback Period = $300/($200 x 0.60) = 2.5

Based on the resulting 2.5 figure, it takes, on average, 2.5 months of profit from the newly acquired customers to pay for the customer’s acquisition cost.

Understanding CAC Payback Period Efficiency

If it’s less than 12 months, it’s favorable. This implies a business has an efficient approach to profitability and growth. However, it’s not a hard and fast rule because the repayment time frame can fluctuate based on the economy and the business operations. If a company is a low-margin business or industry (e-commerce, groceries, etc.), a far tighter payback time frame would be necessary to be viable.

There are many factors that can affect this company-specific measurement, such as the industry or sector, current economic conditions, or the business’ approach to gaining new customers. If a company has a shorter CAC Payback Period in an industry that has a generally accepted longer one, this can imply that the company is more efficient in its operations.

This metric is another tool in a financial analyst’s toolbox that can measure and identify efficiency (or lack thereof) and help put businesses back on track for greater financial health.

Calculating the CAC Payback Period

January 1, 2025 · Blog, General Business News

⏱ 4 min read

The CAC Payback Period looks at how a business needs to recover its investment in attracting new customers. It is especially crucial for companies that are in industries with large marketing and sales costs. It’s an important metric because it helps businesses measure their performance in a number of ways.

First, it shows how well a business is managing its budget. Based on the resulting figure of the CAC Payback Period, the shorter the time required to break even on its customer acquisition costs, the more efficient a company is with its sales and marketing expenses. If, however, the result is high, this signals the company is doing something wrong and needs to analyze its current approach.

Running this analysis can also identify a company’s financial perils. The more prolonged the CAC Payback Period, the more likely a company might be facing cash flow concerns. Whether it is caused by overall economic conditions or industry or company-specific challenges, this is another reason for a company to run the numbers to see how it can mitigate or turn around the costs associated with acquiring customers.

The calculation also can help a business determine if it is able to expand to new products and markets and scale up existing product lines. The shorter the time needed to acquire new customers, the more likely a business can grow.

When investors and lenders analyze a company’s financials, including this metric, the more efficient a company is, and the more likely it will attract investors or have lenders offer favorable financing terms.

How to Calculate the CAC Payback Period

This scenario looks at $300,000 in customer acquisition costs, such as marketing, sales, etc., for a three-month period. The company obtained 1,000 new customers and is expected to gain $200,000 in new monthly recurring revenue (MRR), with an estimated gross margin of 60 percent.

First Step: Calculate the CAC by dividing Sales and Marketing Expenses by the new customers (1,000). It’s expressed as follows:

CAC = Sales and Marketing Expenses/Number of New Customers

CAC = $300,000/1,000 = $300 per customer

Second Step: This is to determine the monthly recurring revenue (MRR) per customer. The new MRR amount is divided by the number of newly acquired customers. It’s calculated as follows:

MRR = $200,000/1,000 = $200 per customer

Third Step: Determine the gross margin or how much remains from revenue after subtracting direct costs. In this case, we’ll use 60 percent.

Fourth (and Final) Step: This step determines how many months it will take to recoup the customer acquisition costs from the profits generated by the newly acquired customer. It’s calculated as follows:

CAC Payback Period = $300/($200 x 0.60) = 2.5

Based on the resulting 2.5 figure, it takes, on average, 2.5 months of profit from the newly acquired customers to pay for the customer’s acquisition cost.

Understanding CAC Payback Period Efficiency

If it’s less than 12 months, it’s favorable. This implies a business has an efficient approach to profitability and growth. However, it’s not a hard and fast rule because the repayment time frame can fluctuate based on the economy and the business operations. If a company is a low-margin business or industry (e-commerce, groceries, etc.), a far tighter payback time frame would be necessary to be viable.

There are many factors that can affect this company-specific measurement, such as the industry or sector, current economic conditions, or the business’ approach to gaining new customers. If a company has a shorter CAC Payback Period in an industry that has a generally accepted longer one, this can imply that the company is more efficient in its operations.

This metric is another tool in a financial analyst’s toolbox that can measure and identify efficiency (or lack thereof) and help put businesses back on track for greater financial health.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

The Social Security Fairness Act of 2023, formally known as H.R. 82, aimed at ending two provisions in the Social Security system that affect public sector employees who have earned pensions from jobs not covered by Social Security. These provisions are the Windfall Elimination Provision and the Government Pension Offset, both of which reduce or eliminate Social Security benefits for workers who have worked in both public-sector and private-sector jobs.

The Problem: WEP and GPO

The Windfall Elimination Provision and the Government Pension Offset were originally designed to prevent public sector workers from receiving larger Social Security benefits than they would have been entitled to had they worked in jobs covered by Social Security for their entire careers. However, critics argue that these provisions disproportionately harm workers who have spent a significant portion of their careers in public service, such as teachers, police officers, firefighters, and other state and local government employees.

Windfall Elimination Provision (WEP):

The WEP reduces the Social Security benefits of individuals who have worked in both the private sector (where they paid into Social Security) and the public sector (where they often did not contribute to Social Security). Typically, Social Security benefits are based on an individual’s 35 highest-earning years. The WEP alters the formula used to calculate benefits for individuals with fewer than 30 years of substantial earnings in Social Security-covered employment, leading to a lower Social Security benefit than they would otherwise be entitled to. For many, this results in a significant reduction in the monthly payment they would have received under the standard Social Security formula.

Government Pension Offset (GPO):

The GPO affects spouses and widows/widowers of Social Security beneficiaries. Under this provision, individuals who receive a government pension from work that was not covered by Social Security (such as state or local government employees) see a reduction in their spousal or survivor benefits from Social Security. The offset is calculated by reducing the spousal or survivor benefit by an amount equal to two-thirds of the government pension. This can leave many public employees with little to no spousal or survivor benefits despite their spouse having paid into Social Security.

What H.R. 82 Seeks to Accomplish

By eliminating both the WEP and GPO, the bill aims to ensure that public sector workers who have earned Social Security benefits through their work in the private sector are not penalized by reductions in those benefits. It also seeks to provide fairer treatment for the spouses and survivors of government employees who may otherwise see their Social Security benefits reduced or eliminated entirely.

The bill has garnered bipartisan support, as lawmakers from both sides of the aisle recognize the fairness of eliminating these provisions, which many see as an unjust penalty against those who have dedicated their careers to public service. H.R. 82, if passed, would provide much-needed relief to millions of retirees, many of who are struggling with the financial impacts of these provisions.

Conclusion:

The introduction of H.R. 82, the Social Security Fairness Act of 2023, marks a crucial point in the ongoing debate over Social Security benefits for public sector workers. By eliminating the Windfall Elimination Provision and the Government Pension Offset, the bill would restore fairness and equity for millions of public employees who have spent their careers in service to their communities. As this bill progresses, it will likely remain a significant issue in discussions surrounding Social Security reform and the treatment of public sector employees.

President Joe Biden signed H.R. 82, the Social Security Fairness Act, into law on Sunday, January 5, 2025, at 3:00 p.m. Central Time Zone.

The Social Security Fairness Act of 2023: More Retirement Income for Teachers, Police, Firefighters & Gov. Workers

January 1, 2025 · Blog, Guest Article of the Month

⏱ 3 min read

The Social Security Fairness Act of 2023, formally known as H.R. 82, aimed at ending two provisions in the Social Security system that affect public sector employees who have earned pensions from jobs not covered by Social Security. These provisions are the Windfall Elimination Provision and the Government Pension Offset, both of which reduce or eliminate Social Security benefits for workers who have worked in both public-sector and private-sector jobs.

The Problem: WEP and GPO

The Windfall Elimination Provision and the Government Pension Offset were originally designed to prevent public sector workers from receiving larger Social Security benefits than they would have been entitled to had they worked in jobs covered by Social Security for their entire careers. However, critics argue that these provisions disproportionately harm workers who have spent a significant portion of their careers in public service, such as teachers, police officers, firefighters, and other state and local government employees.

Windfall Elimination Provision (WEP):

The WEP reduces the Social Security benefits of individuals who have worked in both the private sector (where they paid into Social Security) and the public sector (where they often did not contribute to Social Security). Typically, Social Security benefits are based on an individual’s 35 highest-earning years. The WEP alters the formula used to calculate benefits for individuals with fewer than 30 years of substantial earnings in Social Security-covered employment, leading to a lower Social Security benefit than they would otherwise be entitled to. For many, this results in a significant reduction in the monthly payment they would have received under the standard Social Security formula.

Government Pension Offset (GPO):

The GPO affects spouses and widows/widowers of Social Security beneficiaries. Under this provision, individuals who receive a government pension from work that was not covered by Social Security (such as state or local government employees) see a reduction in their spousal or survivor benefits from Social Security. The offset is calculated by reducing the spousal or survivor benefit by an amount equal to two-thirds of the government pension. This can leave many public employees with little to no spousal or survivor benefits despite their spouse having paid into Social Security.

What H.R. 82 Seeks to Accomplish

By eliminating both the WEP and GPO, the bill aims to ensure that public sector workers who have earned Social Security benefits through their work in the private sector are not penalized by reductions in those benefits. It also seeks to provide fairer treatment for the spouses and survivors of government employees who may otherwise see their Social Security benefits reduced or eliminated entirely.

The bill has garnered bipartisan support, as lawmakers from both sides of the aisle recognize the fairness of eliminating these provisions, which many see as an unjust penalty against those who have dedicated their careers to public service. H.R. 82, if passed, would provide much-needed relief to millions of retirees, many of who are struggling with the financial impacts of these provisions.

Conclusion:

The introduction of H.R. 82, the Social Security Fairness Act of 2023, marks a crucial point in the ongoing debate over Social Security benefits for public sector workers. By eliminating the Windfall Elimination Provision and the Government Pension Offset, the bill would restore fairness and equity for millions of public employees who have spent their careers in service to their communities. As this bill progresses, it will likely remain a significant issue in discussions surrounding Social Security reform and the treatment of public sector employees.

President Joe Biden signed H.R. 82, the Social Security Fairness Act, into law on Sunday, January 5, 2025, at 3:00 p.m. Central Time Zone.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

Whether you file your income tax return early or at the last minute, there are ways to simplify the process and reduce what you owe – or even increase your refund – before the deadline.

Filing Simplification Tip

Once you receive your W-2 and/or 1099 tax forms, see what income tax bracket you fall under to determine whether you should itemize expenses or take the standard deduction. Thinking about this step first can save you a lot of time. If you don’t come near the standard deduction amount, you will not be itemizing expenses. And if you are not itemizing expenses, you won’t have to gather all the receipts (e.g., mortgage interest, property tax, state and local income taxes, and sales tax paid in 2024).

2024 Tax Season Income Tax Brackets

Single filer

Married filing separately

Married filing jointly (includes qualifying widow/er)

Head of Household

Tax Rate

$0 to $11,600

$0 to $11,600

$0 to $23,200

$0 to $16,550

10%

$11,601 to $47,150

$11,601 to $47,150

$23,201 to $94,300

$16,551 to $63,100

12%

$47,151 to $100,525

$47,151 to $100,525

$94,301 to $201,050

$63,101 to $100,500

22%

$100,526 to $191,950

$100,526 to $191,950

$201,051 to $383,900

$100,501 to $191,950

24%

$191,951 to $243,725

$191,951 to $243,725

$383,901 to $487,450

$191,951 to $243,700

32%

$243,726 to $609,350

$243,726 to $365,600

$487,451 to $731,200

$243,701 to $609,350

35%

$609,351 or more

$365,601 or more

$731,201 or more

$609,351 or more

37%

2024 Tax Season Standard Deductions

Single filer and married filing separately

Married filing jointly (includes qualifying widow/er)

Head of Household

$14,600

$29,200

$21,900

Retirement Saving Tips

It’s not too late to contribute to an IRA. Both the traditional and Roth IRAs allow you to make contributions for 2024 up until the tax-filing deadline of the following year – which this year is Tuesday, April 15. The advantage to this later deadline is that you can complete your taxes before they are due, then adjust them to reduce your tax liability if needed by contributing to your IRA. The total maximum contribution you can make to all of your IRAs combined (both Roths and traditional) is $7,000 for 2024 or $8,000 if you are 50 years or older.

However, if you have a Roth IRA, there are restrictions to contributions based on your 2024 income. You may make the maximum contribution to your Roth only if your 2024 modified adjusted gross income (MAGI) is less than a certain threshold.

Filing Status

MAGI

Contribution amount

Single and Head of Household filers

Below $146,000

Between $146,001 and 161,000

Above $161,000

$7,000/$8,000 (age 50+)

Phased (IRS Worksheet 2-2)

Nothing

Married filing jointly

(includes qualifying widow/er)

Below $230,000

Between $230,000 and $240,000

Above $240,000

$7,000/$8,000 (age 50+)

Phased (IRS Worksheet 2-2)

Nothing

Be aware that the amount of deduction you can claim for a traditional IRA contribution may be limited if you or your spouse are covered by a retirement plan at work.

Filing Status

MAGI

Deduction amount

Single and Head of Household filers

$77,000 or less

Between $77,000 and 87,000

$87,000 or more

Full deduction

Partial (IRS Worksheet 1-2)

None

Married filing jointly

(includes qualifying widow/er)

$123,000 or less

Between $123,000 and 143,000

$143,000 or more

Full deduction

Partial (IRS Worksheet 1-2)

None

Married filing separately

Less than $10,000

$10,000 or more

Partial (IRS Worksheet 1-2)

None

If you make a traditional and/or Roth IRA contribution by the April 15 deadline, you may qualify for the Retirement Saver’s Credit (also available if you contributed to an employer plan by Dec. 31, 2024). The maximum credit is $1,000 ($2,000 for married couples), and it can increase your refund or reduce the tax you owe. However, the saver’s credit is subject to other deductions, credits, and income restrictions.

Filing Status

MAGI

Single and Married filing separately

up to $57,375

Married couples filing jointly

(includes qualifying widow/er)

up to $76,500

Head of Household Filers

up to $57,375

Work with an experienced tax preparer to take advantage of legitimate deductions and credits to ensure that you only pay what is required for your situation.

Tips for Tax Season

January 1, 2025 · Blog, Financial Planning

⏱ 4 min read

Whether you file your income tax return early or at the last minute, there are ways to simplify the process and reduce what you owe – or even increase your refund – before the deadline.

Filing Simplification Tip

Once you receive your W-2 and/or 1099 tax forms, see what income tax bracket you fall under to determine whether you should itemize expenses or take the standard deduction. Thinking about this step first can save you a lot of time. If you don’t come near the standard deduction amount, you will not be itemizing expenses. And if you are not itemizing expenses, you won’t have to gather all the receipts (e.g., mortgage interest, property tax, state and local income taxes, and sales tax paid in 2024).

2024 Tax Season Income Tax Brackets

Single filer

Married filing separately

Married filing jointly (includes qualifying widow/er)

Head of Household

Tax Rate

$0 to $11,600

$0 to $11,600

$0 to $23,200

$0 to $16,550

10%

$11,601 to $47,150

$11,601 to $47,150

$23,201 to $94,300

$16,551 to $63,100

12%

$47,151 to $100,525

$47,151 to $100,525

$94,301 to $201,050

$63,101 to $100,500

22%

$100,526 to $191,950

$100,526 to $191,950

$201,051 to $383,900

$100,501 to $191,950

24%

$191,951 to $243,725

$191,951 to $243,725

$383,901 to $487,450

$191,951 to $243,700

32%

$243,726 to $609,350

$243,726 to $365,600

$487,451 to $731,200

$243,701 to $609,350

35%

$609,351 or more

$365,601 or more

$731,201 or more

$609,351 or more

37%

2024 Tax Season Standard Deductions

Single filer and married filing separately

Married filing jointly (includes qualifying widow/er)

Head of Household

$14,600

$29,200

$21,900

Retirement Saving Tips

It’s not too late to contribute to an IRA. Both the traditional and Roth IRAs allow you to make contributions for 2024 up until the tax-filing deadline of the following year – which this year is Tuesday, April 15. The advantage to this later deadline is that you can complete your taxes before they are due, then adjust them to reduce your tax liability if needed by contributing to your IRA. The total maximum contribution you can make to all of your IRAs combined (both Roths and traditional) is $7,000 for 2024 or $8,000 if you are 50 years or older.

However, if you have a Roth IRA, there are restrictions to contributions based on your 2024 income. You may make the maximum contribution to your Roth only if your 2024 modified adjusted gross income (MAGI) is less than a certain threshold.

Filing Status

MAGI

Contribution amount

Single and Head of Household filers

Below $146,000

Between $146,001 and 161,000

Above $161,000

$7,000/$8,000 (age 50+)

Phased (IRS Worksheet 2-2)

Nothing

Married filing jointly

(includes qualifying widow/er)

Below $230,000

Between $230,000 and $240,000

Above $240,000

$7,000/$8,000 (age 50+)

Phased (IRS Worksheet 2-2)

Nothing

Be aware that the amount of deduction you can claim for a traditional IRA contribution may be limited if you or your spouse are covered by a retirement plan at work.

Filing Status

MAGI

Deduction amount

Single and Head of Household filers

$77,000 or less

Between $77,000 and 87,000

$87,000 or more

Full deduction

Partial (IRS Worksheet 1-2)

None

Married filing jointly

(includes qualifying widow/er)

$123,000 or less

Between $123,000 and 143,000

$143,000 or more

Full deduction

Partial (IRS Worksheet 1-2)

None

Married filing separately

Less than $10,000

$10,000 or more

Partial (IRS Worksheet 1-2)

None

If you make a traditional and/or Roth IRA contribution by the April 15 deadline, you may qualify for the Retirement Saver’s Credit (also available if you contributed to an employer plan by Dec. 31, 2024). The maximum credit is $1,000 ($2,000 for married couples), and it can increase your refund or reduce the tax you owe. However, the saver’s credit is subject to other deductions, credits, and income restrictions.

Filing Status

MAGI

Single and Married filing separately

up to $57,375

Married couples filing jointly

(includes qualifying widow/er)

up to $76,500

Head of Household Filers

up to $57,375

Work with an experienced tax preparer to take advantage of legitimate deductions and credits to ensure that you only pay what is required for your situation.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

All bills not enacted by the end of the 118th congressional session on Jan. 3, 2025, will expire.

Social Security Fairness Act of 2023 (HR 82) – This bill, with 330 bipartisan sponsors and a similar bill in the Senate, was introduced by Rep. Garret Graves (R-LA) on Jan. 9, 2023. It passed in the House on Nov. 12 of this year and is likely to pass in the Senate before the year’s end. The purpose of the bill is to eliminate the government pension offset that reduces Social Security benefits for individuals who receive other benefits, such as a pension from a state or local government. In the private sector, this would have a similar effect to withholding Social Security from people who have a 401(k). The bill would also repeal provisions that reduce Social Security benefits for spouses and widows/ers who receive their own government pensions. The provisions of the bill would be retroactive to the beginning of 2024.

BOLIVAR Act (HR 825) – This legislation prohibits the head of an executive agency to enter into a contract for the procurement of goods or services with any person that has business operations with the Maduro regime in Venezuela. The act was introduced on Feb. 2, 2023, by Rep. Michael Waltz (R-OH). It passed in the House on Nov. 18, and its fate currently lies with the Senate.

Vote by Mail Tracking Act (HR 5658) – This bill would require mail-in ballots to use the Postal Service barcode and an Official Election Mail logo. It passed in the House on Nov. 18 and is under consideration in the Senate. The bill was introduced by Rep. Katie Porter (D-CA) on Sept. 21, 2023.

Find and Protect Foster Youth Act (S 1146) – This act was introduced on March 30, 2023, by Sen. John Cornyn (R-TX). It would amend a provision of the Social Security Act to require the Department of Health and Human Services to eliminate obstacles to identifying and responding to reports of missing foster care children. Furthermore, it would assist in the assessment and screening of children who are at risk of becoming victims of sex trafficking, as well as identify best practices for effective interventions. The bipartisan bill passed in the House on Nov. 18 and is currently in the Senate.

Billion Dollar Boondoggle Act of 2023 (S 1228) – This bill was introduced by Sen. Joni Ernst (R-IA) on April 25, 2023. The bill would require the director of the Office of Management and Budget to submit an annual report to Congress detailing projects that are over budget and behind schedule. This is a bipartisan bill that has passed in both the Senate and the House, but on July 22, the House made changes and sent it back to the Senate, where it currently resides.

Rural Broadband Protection Act of 2024 (S 275) – Introduced by Sen. Shelley Moore Capito (R-WV) on Feb. 7, 2023, this bill would require the Federal Communications Commission (FCC) to vet applicants for funding of affordable broadband deployment in high-cost areas (including rural communities). The FCC would mandate a process, including a detailed proposal with technical capabilities to provide competitive awards for implementing the broadband network services. The FCC would then assess proposals in line with well-established technical standards. The bill passed the Senate on Sept. 25 and is currently with the House.

Making Pensions Equitable, Protecting Foster Kids, Mail-in Votes and Tracking Government Spending

December 1, 2024 · Blog, Congress at Work

⏱ 3 min read

All bills not enacted by the end of the 118th congressional session on Jan. 3, 2025, will expire.

Social Security Fairness Act of 2023 (HR 82) – This bill, with 330 bipartisan sponsors and a similar bill in the Senate, was introduced by Rep. Garret Graves (R-LA) on Jan. 9, 2023. It passed in the House on Nov. 12 of this year and is likely to pass in the Senate before the year’s end. The purpose of the bill is to eliminate the government pension offset that reduces Social Security benefits for individuals who receive other benefits, such as a pension from a state or local government. In the private sector, this would have a similar effect to withholding Social Security from people who have a 401(k). The bill would also repeal provisions that reduce Social Security benefits for spouses and widows/ers who receive their own government pensions. The provisions of the bill would be retroactive to the beginning of 2024.

BOLIVAR Act (HR 825) – This legislation prohibits the head of an executive agency to enter into a contract for the procurement of goods or services with any person that has business operations with the Maduro regime in Venezuela. The act was introduced on Feb. 2, 2023, by Rep. Michael Waltz (R-OH). It passed in the House on Nov. 18, and its fate currently lies with the Senate.

Vote by Mail Tracking Act (HR 5658) – This bill would require mail-in ballots to use the Postal Service barcode and an Official Election Mail logo. It passed in the House on Nov. 18 and is under consideration in the Senate. The bill was introduced by Rep. Katie Porter (D-CA) on Sept. 21, 2023.

Find and Protect Foster Youth Act (S 1146) – This act was introduced on March 30, 2023, by Sen. John Cornyn (R-TX). It would amend a provision of the Social Security Act to require the Department of Health and Human Services to eliminate obstacles to identifying and responding to reports of missing foster care children. Furthermore, it would assist in the assessment and screening of children who are at risk of becoming victims of sex trafficking, as well as identify best practices for effective interventions. The bipartisan bill passed in the House on Nov. 18 and is currently in the Senate.

Billion Dollar Boondoggle Act of 2023 (S 1228) – This bill was introduced by Sen. Joni Ernst (R-IA) on April 25, 2023. The bill would require the director of the Office of Management and Budget to submit an annual report to Congress detailing projects that are over budget and behind schedule. This is a bipartisan bill that has passed in both the Senate and the House, but on July 22, the House made changes and sent it back to the Senate, where it currently resides.

Rural Broadband Protection Act of 2024 (S 275) – Introduced by Sen. Shelley Moore Capito (R-WV) on Feb. 7, 2023, this bill would require the Federal Communications Commission (FCC) to vet applicants for funding of affordable broadband deployment in high-cost areas (including rural communities). The FCC would mandate a process, including a detailed proposal with technical capabilities to provide competitive awards for implementing the broadband network services. The FCC would then assess proposals in line with well-established technical standards. The bill passed the Senate on Sept. 25 and is currently with the House.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

The holiday season is when most people go on shopping sprees and travel. This season also witnesses a surge in online activities in today’s digital world. Unfortunately, cybercriminals take advantage of this period to launch attacks. Therefore, cybersecurity should be the top priority for a business gearing up for peak sales or a shopper looking for the best deal.

Understanding Holiday Cyber Threats

Businesses and consumers face unique challenges during the holiday season. For businesses, the increase in traffic and online transactions can overwhelm systems. This may make them vulnerable to attacks. Cybercriminals may use tactics such as ransomware, phishing scams and fraudulent transactions during the busy season. Consumers, on the other hand, get lured by malicious ads, fake websites and phishing emails that may appear as irresistible holiday deals.

Recognizing these risks is important to staying safe for both businesses and consumers. Understanding them also means taking proactive measures to reduce exposure to cyber threats.

Why Cybersecurity Matters

The lack of effective cybersecurity can lead to financial loss, reputational damage and disruption to a businesses’ operations. On the other hand, consumers face identity theft, unauthorized purchases and compromised financial accounts.

According to the Retail and Hospitality Information Sharing and Analysis Center (RH-ISAC), threats such as ransomware, phishing, and account takeover (ATO) attacks intensify as consumer activity surges. In their 2024 Holiday Season Cyber Threat Trends Report, RH-ISAC emphasizes proactive defense measures, especially during high-traffic periods like the holiday season.

Cybersecurity Best Practices for Businesses

Security measures for businesses include:

Set up a holiday strategy – over the long holidays, businesses tend to have a change in work schedules and fewer staff members. Having a holiday cybersecurity strategy can safeguard against potential cyber threats. This can include an emergency response plan and designating responsible individuals for cybersecurity.

Endpoint security – this involves protecting devices like computers and smartphones used in the business. It is important to update all software, install antivirus programs and enable firewalls to shield the business network from intrusions.

Employee training – human error is one of the leading causes of data breaches. Therefore, it is important to educate staff to recognize phishing attempts. They should also know the importance of strong passwords and reporting suspicious activity.

Monitoring systems for unusual activity – This requires a business to invest in tools that help detect suspicious behavior in its networks. This should include fraud detection systems that will help identify unusual transaction patterns. It also helps detect potential compromises from third-party vendors.

Backup and recovery plan – business continuity in case of an attack is crucial. Therefore, a business should ensure that data is regularly backed up and stored securely. It also helps to test the recovery process regularly.

Cybersecurity Best Practices for Shoppers

Consumers are not immune to holiday cyber-attacks. A consumer must keep the following in mind:

Shop from secure websites – shoppers should be cautious by checking website security. They should check that a website includes “https://” and a padlock icon in the URL. Also, confirm the correct name of the website. It is also important to avoid clicking on links from unsolicited emails or social media ads. This is a common phishing tactic.

Use secure payment methods – a credit card provides better fraud protection than a debit card. Consider digital wallets that have an extra layer of encryption. It is also crucial to avoid saving payment details on websites.

Avoid public wi-fi – shopping on the go may see some shoppers use public networks. These networks expose data to hackers.

Be wary of emails and messages with deals that sound too good to be true. Always verify sender authentication and, where necessary, contact the company directly.

Be cautious about unexpected package notifications. Unexpected package notifications can be a phishing tactic to steal personal information or install malware. Always verify the sender and avoid clicking on links in unsolicited messages.

Be cautious of holiday scams like fake charities, gift card scams and fake gift exchanges that prey on the season’s generosity and excitement. Scammers may trick customers into buying gift cards or sharing personal details through fraudulent schemes. Staying skeptical of unsolicited offers and never sharing sensitive information with unverified sources will help ward off cybercriminal attacks.

Activate multi-factor authentication (MFA) – adding MFA creates an extra layer of security for highly sensitive accounts such as email, bank, and work-related logins.

Closing Thoughts

The holiday season is meant to be a time of celebration and connection, not worry and stress. By implementing robust cybersecurity practices, businesses can protect their operations and customers while shoppers enjoy safe, hassle-free transactions.

Cybersecurity Best Practices for the Holiday Season

December 1, 2024 · Blog, What's New in Technology

⏱ 4 min read